Paul Morigi

Overview

I lately learn an article that said Warren Buffett does not purchase actual property within the headline. Moreover, within the article it said Warren Buffett did not amass his fortune by shopping for actual property. After studying additional, the article’s major level was there are autos to realize publicity to actual property equivalent to REITs. I fully agree. Within the following piece, I’ll debunk the assertion that Warren Buffett doesn’t purchase actual property and actual property has not helped him amass his fortune, simply to set the report straight. I’ll then give my high REIT decide as of at the moment. First let’s handle the “Warren Buffett does not purchase actual property” and “hasn’t amassed his fortune from actual property” statements.

Buffett does not purchase actual property? I urge to vary.

This assertion could not be farther from the reality. As a devoted follower of Warren Buffett’s investing exploits and being in the true property enterprise as a house builder and licensed Texas realtor for the previous 21 years, I can inform you that Warren Buffett has in all probability purchased extra actual property that every other investor on earth so far. Warren Buffett’s Berkshire Hathaway (BRK.B) (BRK.A) purchased Clayton Properties in 2002 for an all-cash supply.

I already know what you’re going to say subsequent. Berkshire Hathaway will not be Warren Buffett. Effectively, the very fact of the matter is Warren Buffett personally recognized and negotiated the acquisition of Clayton properties by Berkshire, and it is truly a really attention-grabbing story.

Warren Buffett’s Clayton Properties Purchase

So, sure Warren Buffett himself negotiated and acquired Clayton Properties for an all-cash deal. Clayton Properties is now a subsidiary of Berkshire Hathaway. In 2002, Clayton Properties earned revenues of $1.2 billion. It was acquired by Berkshire Hathaway in 2003 for $1.7 billion. Buffett had already dipped a toe into the manufactured-housing market by investing greater than $200 million within the debt of Oakwood Properties on the time. The way in which Warren Buffett turned conscious of Clayton Properties is definitely a darn good yarn. What started as a cordial assembly shortly become one among Buffett’s hardest acquisitions. Let me clarify.

Buffett’s Clayton Properties Purchase backstory

College of Tennessee finance professor Al Auxier, and 40 members of the varsity’s Monetary Administration Affiliation had flown to Omaha to go to Warren Buffett himself, due to a relationship cultivated through the years by Auxier.

Clayton Properties, is headquartered simply outdoors Knoxville, in neighboring Maryville. Professor Auxier and Jim Clayton, the CEO of Clayton Properties on the time have been pals. The group gave Buffett a replica of Clayton’s e-book “First a Dream” Clayton’s autobiography detailing his rise from the son of a cotton farmer to a mainstay on the Forbes 400 listing of the wealthiest People because the founding father of Clayton Properties. Because the legend goes, Buffett was so impressed by Jim Clayton’s e-book that he determined to purchase his firm. Over the previous 20 years Clayton Properties has grown by acquisition and organically to grow to be the most important homebuilder in the USA, accounting for roughly half the business’s whole.

Clayton Properties is now the most important US house builder

As of 2019, Clayton Properties has 40 house constructing services and greater than 350 stores situated throughout the USA. The corporate employs 16,000 folks and produces about 50,000 properties per 12 months at its services, which is about half of the business’s whole. Anybody who’s in the true property business is aware of very effectively Warren Buffett buys actual property and actual property has been a key consider how he has amassed his wealth. Now that we’ve debunked the diatribe that Buffett does not purchase actual property, let’s transfer on to the precise focus of this text. What REIT at present presents a shopping for alternative? Effectively, as destiny would have it, Warren Buffett truly owns much more actual property within the type of the REIT STORE Capital Company (NYSE:STOR), which I’ve on my watchlist as a strong retirement earnings shopping for alternative. Let’s focus on.

Berkshire’s STORE Capital purchase

Berkshire Hathaway invested $377 million in STORE Capital, representing 9.8% of whole shares excellent in 2017. Berkshire now holds 14.7 million shares for $417 million representing a 5.3% stake within the REIT.

About Retailer Capital

STORE Capital targets triple-net lease Single-Tenant Operational Actual Property properties. Beneath this mannequin, STORE buys the properties from enterprise house owners after which leases them again to the house owners.

Prime Prospects (In search of Alpha)

Beneath a triple-net lease plan, the enterprise proprietor/tenant is answerable for maintaining the property in fine condition, making repairs and renovations, and protecting the insurance coverage, property taxes, and different bills.

STORE Prospects (In search of Alpha)

The corporate has been rising its funding portfolio and earnings as effectively. Adjusted funds from operations (FFO) got here in at near $158 million within the first quarter of 2022, up about $32 million 12 months over 12 months.

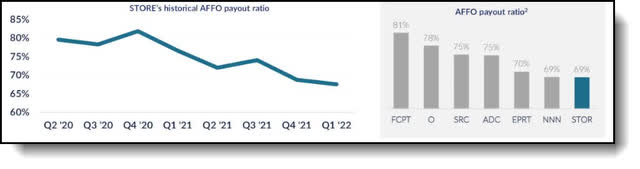

STORE Payout Ratio

AFFO Payout Ratio (In search of Alpha)

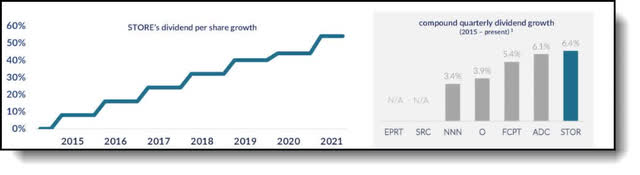

STORE Dividend Per Share Development

Dividend Development (In search of Alpha)

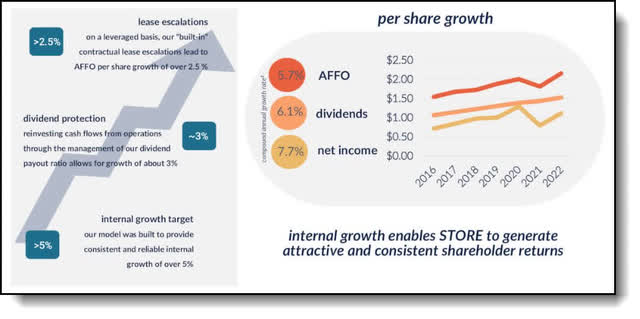

Per Share Development (In search of Alpha)

Whole income additionally grew from roughly $182 million within the first quarter of 2021 to about $222 million within the first quarter of 2022. CEO Mary Fedewa truly raised steerage for the complete 12 months of 2022 over the last earnings name. CEO Mary Fedewa said:

“In gentle of our first quarter efficiency, we’re elevating our acquisition and AFFO steerage for the 12 months. Sherry will present this up to date steerage for 2022 in her remarks. We’ll then open the decision to questions.

Our momentum from 2021 has continued by the primary quarter of 2022. We acquired $513 million in revenue heart actual property, the very best first quarter quantity in STORE’s historical past. These acquisitions have been at an preliminary cap price of seven.1% with weighted common annual lease escalations of 1.8%. Cap charges have been proper according to our steerage. And our funding unfold for the quarter was strong at roughly 340 foundation factors above our current debt issuance.

This exercise, together with the robust efficiency of our portfolio, in strong AFFO of $158 million and AFFO per share of $0.57 for the quarter. Each have been the very best in our historical past and have had a constant upward pattern for the previous 4 quarters.”

Presently the valuation of STORE’s shares are fairly cheap. With STORE guiding for adjusted FFO to return in at $2.20 on the midpoint of its vary in 2022, which means the inventory is buying and selling at about 12.5 occasions ahead adjusted FFO. Furthermore, the REIT’s tenant base is very diversified, rising the margin of security considerably.

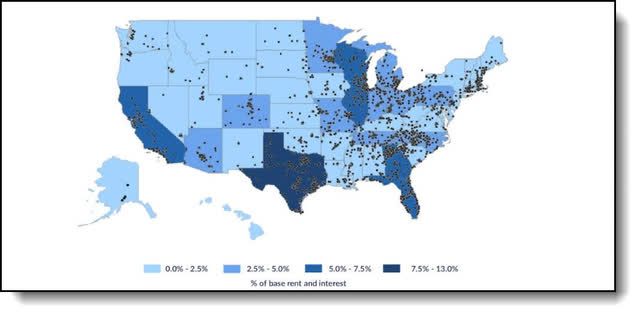

Geographically Numerous

Geographically Numerous (In search of Alpha)

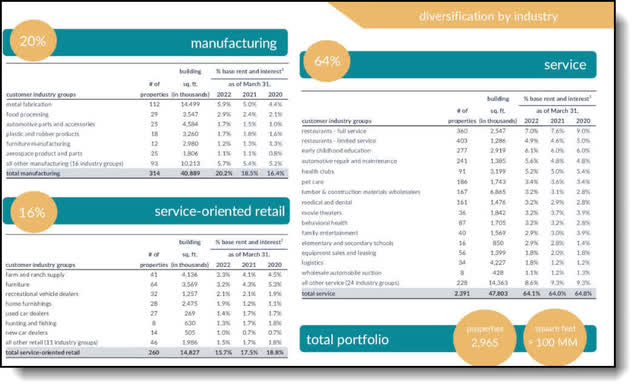

Extremely diversified by business

Diversified By Business (In search of Alpha)

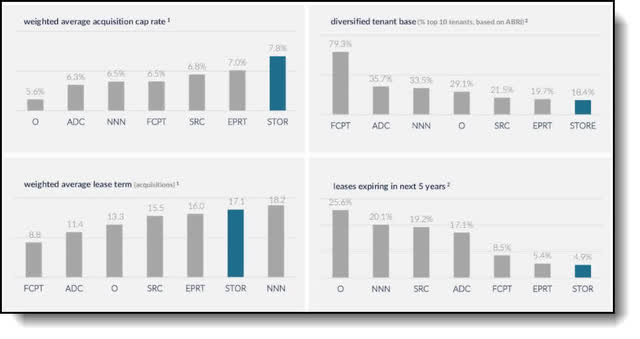

STORE’s funding method ends in engaging cap charges, diversification and lease period.

Diversified Cap Charges and Period (In search of Alpha)

Now let’s wrap this up.

Key Takeaway

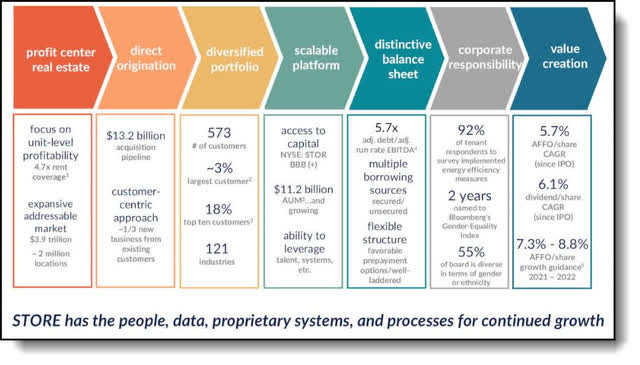

Even within the present atmosphere of rising rates of interest and inflation, STORE has the power to drive development with engaging spreads. STORE’s whole addressable market is estimated to be roughly $4 trillion unfold over two million properties. With such an unlimited whole addressable market, STORE is ready to be extremely selective and select solely the businesses that characterize important, sustainable and rising industries. With such a big whole addressable market alternative STORE has a particularly lengthy runway to develop by choosing solely the best-in-class enterprise alternatives.

STORE Is A Finest-In-Class REIT (In search of Alpha)

Considered one of STORE’s strategic benefits has all the time been its means to establish and efficiently purchase a big quantity of granular transactions. This has been the corporate’s constant technique since its inception. The method permits STORE to cost new leases from each a cap price and lease escalation perspective which permits the corporate to account for the impacts of inflation and rising rates of interest.

STORE is a well-diversified, worthwhile REIT that pays a well-covered dividend yielding 5.49%. What’s extra, the corporate has been bought off lately based mostly on the very fact many available in the market at the moment are promoting first and asking questions later with regard to a possible recession on the horizon.

STORE Present Chart (In search of Alpha)

The inventory is at present down 18% year-to-date and 24% off its 52 week excessive. I see 20% upside over the subsequent 12 months coupled with the 5.49% yield that is an roughly 25% whole return over the subsequent 12 months. Even so, there could also be extra draw back forward. Nonetheless, I see the outsized pullback as an indication of some dangerous information might already be priced in. As Warren Buffett himself would say, “Be grasping when others are fearful!” Now that is a correct ending to this piece!

Closing ideas

I hope you loved the article. These are my ideas on the matter, I look ahead to studying yours. Do you assume STORE presents a shopping for alternative presently? Why or why not. The true worth of my articles lies within the prescient feedback offered by the well-versed In search of Alpha members within the feedback part under. As all the time, I counsel layering in to any new positions over time to scale back danger, my investing motto is “persistence equals earnings.” Moreover, use this text as a place to begin in your personal due diligence.